우리가 매일 마주하는 세계는 불확실성으로 가득 차 있습니다. 입자의 미시적인 움직임부터 거시적인 금융 시장의 주가 흐름에 이르기까지, 완벽하게 예측할 수 있는 것은 존재하지 않습니다. 이러한 혼돈 속에서 질서를 찾으려는 인류의 노력은 두 가지 위대한 지적 성취를 낳았습니다. 하나는 리처드 파인만과 앨버트 힙스가 집대성한 양자역학의 경로 적분법이며, 다른 하나는 월스트리트를 지배하는 금융 공학의 옵션 가격 결정 이론입니다.

이 분석을 통해 도출하려는 목표는, 물리적 우주의 확률론적 본질과 금융 시장의 정교한 위험 척도 사이의 깊은 대칭성을 조명하여 불확실성을 계량화하는 통합된 관점을 제시하는 것입니다. 지금부터 물리학의 렌즈를 통해 금융의 미래를 투영하는 여정을 시작해 보겠습니다. 본문의 핵심 논의는 파인만과 앨버트 힙스의 이론의 깊이를 유지하기 위해 영문 형식으로 전개됩니다.

The Fundamental Concepts of Quantum Mechanics

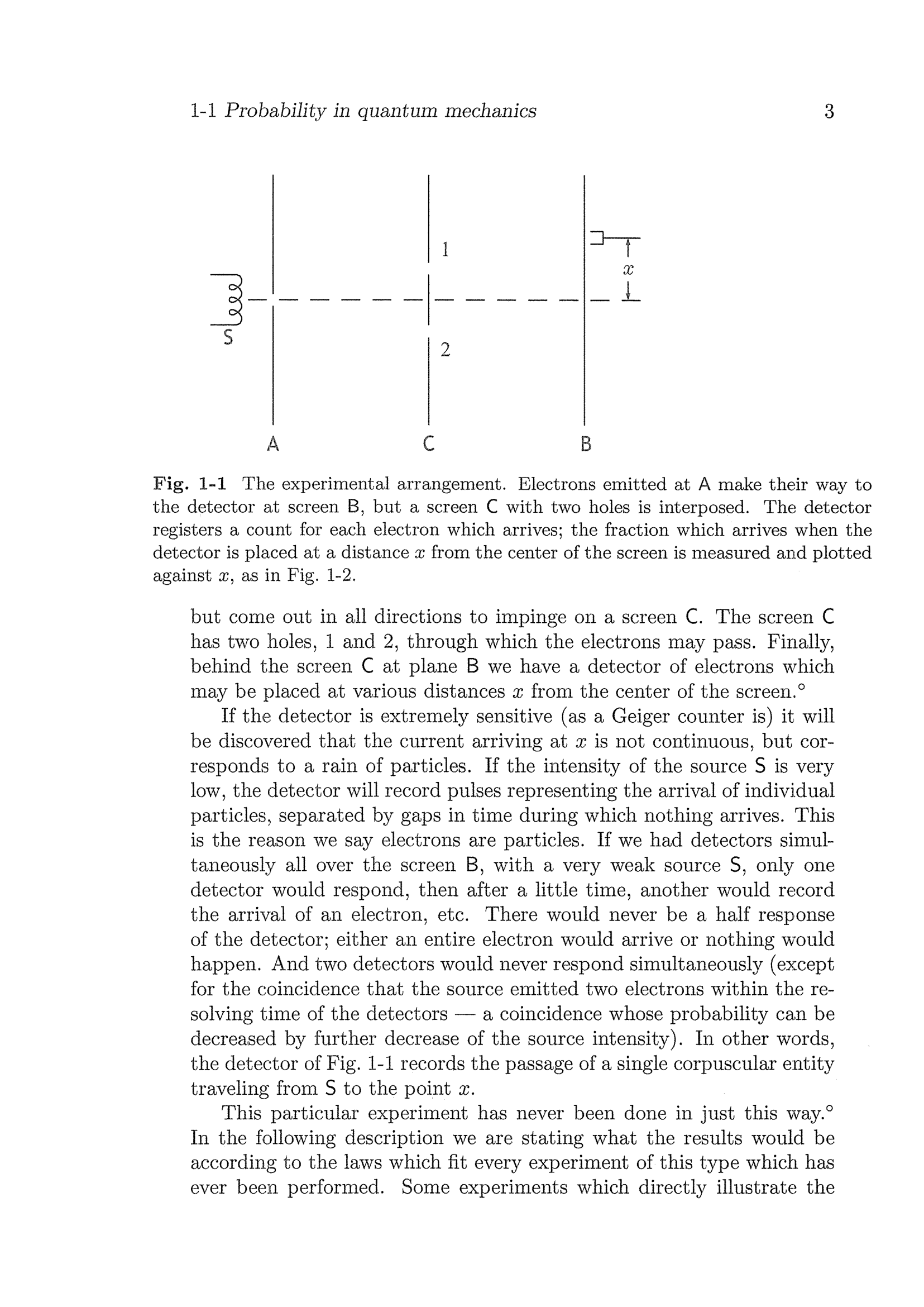

To comprehend the synthesis of quantum mechanics and financial derivatives, one must first dismantle the deterministic worldview inherited from classical mechanics. In the classical paradigm, if the initial position and momentum of a particle are known, its entire future trajectory is flawlessly preordained. However, the foundational premise of quantum mechanics, beautifully elucidated by Richard P. Feynman and Albert R. Hibbs in their seminal work, shatters this illusion. Instead of a single, definitive path, a quantum particle explores an infinite multiplicity of potential trajectories simultaneously. The particle does not travel from point A to point B along a unique route; rather, it 'smells' every conceivable path through spacetime.

This profound shift from determinism to a probabilistic framework is not merely a physical phenomenon but a philosophical revelation. The concept of probability amplitudes replaces absolute certainty. In this quantum realm, the probability of an event is calculated by taking the square of the absolute value of a complex number known as the probability amplitude. When multiple indistinguishable alternatives lead to the same final state, their amplitudes are added together, allowing for the phenomenon of interference. It is a mesmerizing ballet of constructive and destructive interference, where possibilities amplify or cancel each other out before a final measurement is made.

Translating this to the financial ecosystem, the movement of a stock price is inherently stochastic, mimicking the unpredictable nature of a quantum particle. When a financial engineer attempts to price an option—a derivative contract granting the right to buy or sell an asset at a predetermined price in the future—they are not predicting a single future price path. Instead, much like a quantum physicist, they must consider an ensemble of all possible future trajectories the underlying asset might take. The risk-neutral pricing measure acts as the financial equivalent of the probability amplitude, assigning a statistical weight to every single path. Just as the quantum reality is a superposition of all possible physical states, the value of a financial option today is the discounted superposition of all possible economic futures.

The Quantum-mechanical Law of Motion

The ingenuity of Feynman’s approach lies in his formulation of the quantum-mechanical law of motion via the path integral. He postulated that the total probability amplitude for a particle to travel from an initial state (xa, ta) to a final state (xb, tb) is proportional to the sum of the contributions from all conceivable paths connecting these two points. Crucially, the contribution of each individual path is not uniform. It is weighted by a phase factor equal to e(i/ℏ)S, where S is the classical action evaluated along that specific path, i is the imaginary unit, and ℏ is the reduced Planck constant.

The classical action, S, is the time integral of the Lagrangian, representing the difference between kinetic and potential energy. In the macroscopic limit, where the action is massively larger than the quantum of action (Planck's constant), the phase fluctuates wildly for almost all paths. These wild fluctuations lead to immense destructive interference, canceling out the contributions of non-classical paths. The only path that survives this rigorous mathematical winnowing is the path where the action is stationary—this is the principle of least action, which precisely yields the classical trajectory. Thus, Feynman gracefully demonstrated how the classical world emerges as an asymptotic limit of the quantum reality.

In the architecture of modern quantitative finance, the equivalent of the path integral is the expectation value taken under a risk-neutral measure. The financial 'law of motion' is dictated by stochastic differential equations, most notably geometric Brownian motion. While the quantum phase factor is complex and oscillatory, the financial weight assigned to a path is real and exponentially decaying, governed by the Wiener measure. To evaluate the price of an option, one integrates the discounted payoff over the space of all continuous paths the asset could follow. The Feynman-Kac theorem serves as the vital bridge here, formally connecting the probabilistic calculation of expected values over random paths to the solution of deterministic partial differential equations, solidifying the profound structural identity between physical dynamics and market stochastics.

The transition from the oscillating exponential e(i/ℏ)S in physics to the decaying exponential e-rT in finance represents a shift from exploring quantum interference to calculating temporal discounting and risk aversion over an infinite continuum of economic variables.

Developing the Concepts with Special Examples

To solidify the abstract framework of the path integral, Feynman and Hibbs meticulously analyzed special, analytically tractable examples, primarily the free particle and the particle in a uniform gravitational field. For a free particle experiencing no external potential, the action is purely the kinetic energy integrated over time. The calculation of the path integral in this scenario yields a Gaussian kernel. This kernel, mathematically a propagator, dictates exactly how the initial wave function diffuses through space and time.

The mathematical elegance of the free particle propagator is breathtaking. It reveals that in the absence of forces, the spread of the probability amplitude resembles a diffusion process, albeit an imaginary-time one. This fundamental solution is the cornerstone upon which more complex quantum systems are built, serving as the benchmark for understanding how quantum states evolve when unhindered.

This specific Gaussian solution mirrors the most foundational model in option pricing: the geometric Brownian motion of stock prices formulated by Fisher Black, Myron Scholes, and Robert Merton. In their framework, the logarithmic return of a stock price behaves precisely like a 'free particle' undergoing stochastic diffusion. The transition probability density of the stock price from today to the expiration date is a log-normal distribution, which is mathematically isomorphic to the Gaussian propagator of a free quantum particle. When we calculate the price of a standard European call option, we are essentially integrating the option's payoff function against this Gaussian financial propagator. The Black-Scholes formula is, in its purest mathematical essence, a specific, closed-form evaluation of a financial path integral for a free, unconstrained asset.

The Schrödinger Description of Quantum Mechanics

Although Feynman’s path integral approach is revolutionary, it must naturally reconcile with the earlier, highly successful formulation of quantum mechanics: the Schrödinger equation. Feynman meticulously demonstrated that taking the time derivative of the path integral propagator directly yields the time-dependent Schrödinger equation. This partial differential equation describes the continuous, deterministic evolution of the quantum wave function over time. It represents a paradigm where the local, differential perspective of Schrödinger and the global, integral perspective of Feynman are proven to be two sides of the exact same mathematical coin.

The Schrödinger equation is a diffusion equation equipped with an imaginary diffusion constant. It dictates how the probability amplitude flows through configuration space, sculpted by the contours of the potential energy landscape. The wave function, psi(Ψ), encapsulates all ascertainable information about the system, dynamically adjusting itself according to the Hamiltonian operator of the environment.

The parallel in the financial sphere is absolutely uncanny. By applying Ito's Lemma to the stochastic path of a stock and setting up a risk-free hedging portfolio, financial economists derived the Black-Scholes-Merton partial differential equation. This equation governs the evolution of an option's price relative to changes in the underlying asset's price and the passage of time. Structurally, the Black-Scholes PDE is a backward parabolic diffusion equation. If one applies a mathematical transformation known as a Wick rotation—replacing real time with imaginary time—the Schrödinger equation and the Black-Scholes equation become virtually indistinguishable. The potential energy term in quantum mechanics maps perfectly to the risk-free interest rate in finance, and the quantum kinetic energy term corresponds to the asset's volatility.

| Domain | Fundamental Equation | Core Concept |

|---|---|---|

| Quantum Physics | Schrödinger Equation (PDE) | Evolution of probability amplitudes in imaginary time. |

| Quantitative Finance | Black-Scholes-Merton Equation (PDE) | Evolution of derivative prices in backward real time. |

Measurements and Operators

In classical physics, observing a system does not fundamentally alter it. Quantum mechanics, however, introduces a radical departure: the act of measurement actively perturbs the system. A physical observable, such as momentum or position, is represented mathematically by a Hermitian operator acting upon the state vector residing in a Hilbert space. When a measurement is executed, the superposition of the wave function collapses into one of the definite eigenstates of the operator, yielding a specific real-valued eigenvalue as the outcome. The path integral framework accommodates this by inserting operators along the trajectory at the specific moments of observation, effectively altering the sum over histories.

This complex mechanism of observation and operators has a direct and highly practical counterpart in financial derivatives. Consider an exotic derivative contract like an Asian option, whose payoff depends on the average price of the underlying asset over a specified period, or a Barrier option, which activates or extinguishes if the asset price breaches a predetermined level. These contractual conditions are the financial equivalents of quantum measurements.

The payoff function of a derivative contract acts as a financial operator. It takes the abstract, probabilistic distribution of asset paths and collapses them into a tangible cash flow at maturity. In path-dependent options, continuous or discrete 'observations' of the asset price dictate the final payout, perfectly mirroring how a quantum particle is forced into a specific state through continuous observation (the quantum Zeno effect). Evaluating such exotic options requires calculating path integrals where the paths are constrained or modified by the specific 'measurement' rules defined in the derivative's term sheet.

The Perturbation Method in Quantum Mechanics

Nature rarely offers systems that can be solved exactly. To handle the profound complexity of reality, physicists employ perturbation theory. When a quantum system involves a complex potential that defies exact analytical solution, it is split into a solvable unperturbed part and a small perturbing interaction. The solution is then expressed as an infinite series—the Dyson series—where each subsequent term represents an increasingly complex sequence of interactions. Feynman diagrams emerged as an ingenious visual and mathematical tool to calculate these intricate perturbative terms systematically, mapping abstract algebra into intuitive geometric topologies.

The assumption of constant volatility in the Black-Scholes model is an idealization akin to the unperturbed free particle. In reality, market volatility is chaotic; it smiles, it skews, and it reverts to the mean. Financial engineers, confronted with the limitations of the standard model, developed local volatility and stochastic volatility models (like the SABR or Heston models). These sophisticated models are mathematically intractable in closed form.

To price options under these complex realities, quantitative analysts utilize asymptotic expansion and perturbation methods directly inspired by theoretical physics. By treating the variance of volatility (vol of vol) or the mean-reversion speed as a small perturbation parameter, they expand the option price into a power series. The leading term is the standard Black-Scholes price, and the higher-order corrections account for the market's skewness and kurtosis. Financial Feynman diagrams can literally be drawn to track the 'interactions' between the asset price and its underlying volatility process, allowing quants to calculate highly accurate approximations for the prices of complex derivatives in non-Gaussian markets.

Transition Elements

A crucial concept in the text by Feynman and Hibbs is the matrix element, or transition element. This quantifies the probability amplitude for a system to transition from an initial state |i⟩ to a final state |f⟩ under the influence of an operator. In the language of path integrals, it involves calculating the integral over all paths that originate in the initial state and terminate in the final state, weighted by the action and the intervening physical interactions.

These transition amplitudes are the raw materials for calculating cross-sections and decay rates in particle physics. They tell us exactly how likely it is for an electron to scatter off a photon, or for a heavy nucleus to undergo fission. The mathematics is strictly focused on connecting a defined past to an expected future across a turbulent medium.

In the architecture of financial markets, transition elements correspond to state pricing densities, also known as Arrow-Debreu prices. An Arrow-Debreu security is a theoretical contract that pays exactly one dollar if a specific state of the world occurs at a specific time in the future, and zero otherwise. The price of this fundamental security is the financial transition element—it measures the present value of transitioning to that specific economic state. Every complex derivative in the market, no matter how convoluted its term sheet, can be theoretically deconstructed into a linear combination of these elementary transition probabilities. By integrating the product of the derivative's payoff and the state pricing density (the financial propagator), one obtains the fair market value, reflecting a flawless mathematical symmetry with the calculation of quantum observables.

Harmonic Oscillators

The quantum harmonic oscillator is arguably the most important model in all of theoretical physics. It describes a particle subjected to a restoring force proportional to its displacement from equilibrium. Feynman dedicates significant attention to deriving the exact path integral solution for the harmonic oscillator because almost any stable physical system, when slightly perturbed from its minimum energy state, can be approximated as a harmonic oscillator. Its mathematical structure is elegant, yielding discrete, evenly spaced energy levels and the inescapable zero-point energy, a testament to the perpetual jitter of the quantum vacuum.

The financial parallel to the harmonic oscillator is found in the dynamics of interest rates and volatility. Unlike stock prices, which can theoretically grow to infinity, interest rates and volatility exhibit mean-reverting behavior. If interest rates rise too high, central banks intervene, and economic contraction forces them down. If they drop too low, inflation fears drive them back up. This constant pull towards a long-term average is the financial equivalent of the oscillator's restoring force.

Models like the Vasicek model or the Cox-Ingersoll-Ross (CIR) model utilize an Ornstein-Uhlenbeck process to capture this mean reversion. The mathematical formulation of the Ornstein-Uhlenbeck process in stochastic calculus is identical in form to the imaginary-time Schrödinger equation for a quantum harmonic oscillator. Consequently, the pricing formulas for bond options and swaptions involve mathematical functions (like Bessel functions and exponential quadratics) that are mathematically homologous to the wave functions and propagators of the quantum harmonic oscillator derived by Feynman.

Just as physicists use the harmonic oscillator to model atomic vibrations in a crystal lattice, fixed-income traders use mean-reverting stochastic models to price options on the yield curve, relying on the same foundational mathematics.

Quantum Electrodynamics

Feynman's Nobel Prize-winning contribution was his formulation of Quantum Electrodynamics (QED), extending the path integral from single particles to continuous fields. In QED, forces between particles are mediated by the exchange of virtual quanta—for instance, electrons repel each other by exchanging virtual photons. This framework manages the interactions of infinite degrees of freedom, dealing with infinities through a rigorous mathematical process called renormalization. It stands as the most precisely tested theory in the history of science.

When we shift our gaze to the macro-structure of the global financial system, we see a similarly interconnected web of interacting entities. Financial markets are not isolated assets; they are a vast, continuous field of interdependencies. A default in the mortgage market of one country propagates through the banking sector, triggering volatility spikes in global equities and currency fluctuations. The contagion of risk in finance is akin to the propagation of interactions in QED.

To price derivatives on baskets of assets, index options, or Collateralized Debt Obligations (CDOs), financial engineers must model the correlation structures between multiple underlying variables. The application of field-theoretic methods allows for the modeling of systemic risk. Copula functions, used to stitch together marginal distributions into a joint multivariate distribution, serve a function conceptually similar to the interaction vertices in Feynman diagrams, describing how different financial 'fields' couple and influence one another during periods of extreme market stress.

Statistical Mechanics

In the later chapters of the book, Feynman demonstrates a profound mathematical equivalence between quantum mechanics and statistical mechanics. By performing an analytical continuation—replacing time 't' with an imaginary variable '-iℏβ', where β is the inverse temperature—the oscillatory quantum path integral transforms directly into the partition function of classical statistical mechanics. The Schrödinger equation morphs into the heat equation. This implies that calculating the thermodynamic properties of a system at a finite temperature is mathematically identical to calculating the quantum evolution of a system over an imaginary time interval.

This revelation is the ultimate Rosetta Stone connecting physics and quantitative finance. Financial asset paths do not oscillate with complex phases; they diffuse continuously according to real probabilities. By establishing the isomorphism between imaginary-time quantum mechanics and classical diffusion, Feynman inadvertently provided the exact mathematical justification for using physics techniques in finance.

The pricing of an option is mathematically a boundary value problem for a parabolic partial differential equation (the heat equation). The techniques developed by theoretical physicists to calculate partition functions, free energies, and entropies of complex thermodynamic systems are directly ported over by quantitative analysts to calculate present values, Greeks (sensitivities like Delta, Gamma, Vega), and implied volatilities. The option's value is synonymous with the partition function, representing a macroscopic state emerging from an infinite number of microscopic stochastic paths.

The Variational Method

When faced with a quantum system whose ground state energy cannot be calculated exactly, physicists rely heavily on the variational method. This principle states that the expectation value of the Hamiltonian evaluated with any trial wave function will always be greater than or equal to the true ground state energy. By parameterizing a trial wave function and minimizing the energy with respect to those parameters, physicists can obtain highly accurate approximations for complex molecular structures and atomic ground states without solving the exact equations.

In the realm of finance, optimization and finding bounds are daily necessities. The valuation of American options—derivatives that can be exercised at any time prior to expiration—poses a notoriously difficult mathematical problem because it involves determining an optimal early exercise boundary. There is no exact closed-form solution for an American put option.

To conquer this, quantitative engineers utilize variational inequalities and optimal stopping theory. Just as physicists guess a trial wave function, quants guess an optimal exercise boundary. By applying variational principles, they can establish strict upper and lower bounds for the price of the American option. Algorithms like the Longstaff-Schwartz method use least-squares regression across simulated paths to approximate this optimal stopping rule, embodying the very essence of the variational method: iteratively refining an approximation to get as close as possible to an unreachable exact truth.

Other Problems in Probability

In the final sections, the text explores broader applications of path integrals to various problems in classical probability, such as Brownian motion, noise in electronic circuits, and Fokker-Planck equations. Feynman recognized that the formal structure he developed was not limited to the quantum realm but was a universal language for describing stochastic processes.

This universality is what makes the path integral the bedrock of modern financial mathematics. Financial markets are frequently disrupted by extreme events—market crashes, geopolitical shocks, or sudden corporate defaults. The standard geometric Brownian motion fails to capture these discontinuities. To address this, modelers introduce jump-diffusion processes, where continuous diffusion is punctuated by Poisson jumps.

The path integral framework handles these complex probability problems with remarkable agility. By modifying the action functional to include terms representing the probability of jumps, one can construct an integro-differential equation for the option price. Furthermore, for highly path-dependent derivatives, Monte Carlo simulations are employed. A Monte Carlo simulation in finance is literally the numerical evaluation of a Feynman path integral: generating millions of random asset paths, calculating the payoff for each, and averaging them to find the expected value. The theoretical physics of the 1960s has thus become the computational engine of 21st-century global finance.

인터랙티브 분석: 경로 적분 개념을 활용한 옵션 가격 시뮬레이터

물리학의 경로 적분이 금융의 기댓값 계산으로 변환되는 블랙-숄즈 모형의 기본 구조를 브라우저에서 직접 테스트해 보세요. (초기 자산 가격, 행사가, 만기, 무위험 이자율, 변동성을 입력하여 유러피안 콜/풋 옵션 가격을 산출합니다.)

경로 적분과 옵션 가격 융합의 핵심 요약

자주 묻는 질문 (FAQ)

지금까지 물리학의 정수인 양자역학과 금융 시장을 지배하는 옵션 가격 결정 이론이 어떻게 한 뿌리에서 만나 정교한 화음을 이루는지 함께 살펴보았습니다. 자연의 질서를 밝혀낸 선구자들의 우아한 방정식이 수십 년의 시공간을 넘어 오늘날 자본 시장의 위험을 관리하는 든든한 방패가 되었다는 사실은 지식의 진정한 융합이 무엇인지 보여줍니다. 더 깊은 실무 적용에 대해 궁금한 점이 있으시다면 언제든 편하게 질문 남겨주시기 바랍니다.